From 1 July 2021, further legislated changes to super will come into effect. The changes will likely present opportunities across the board for young professionals, pre-retirees and retirees.

Make the most of your retirement savings and identify actions you may need to take to avoid penalties. Find out what you need to know

Super is one of the most tax-effective ways to save for your retirement, and the only way to get money into super is by making contributions. Taking advantage of your available contributions caps each year is important for boosting your super savings. This can help you to be able to live the retirement lifestyle of your choice, and enjoy tax advantages.

Here we share strategies and tips that can help you to boost your retirement savings and make the most of the super changes which come into effect from 1 July 2021.

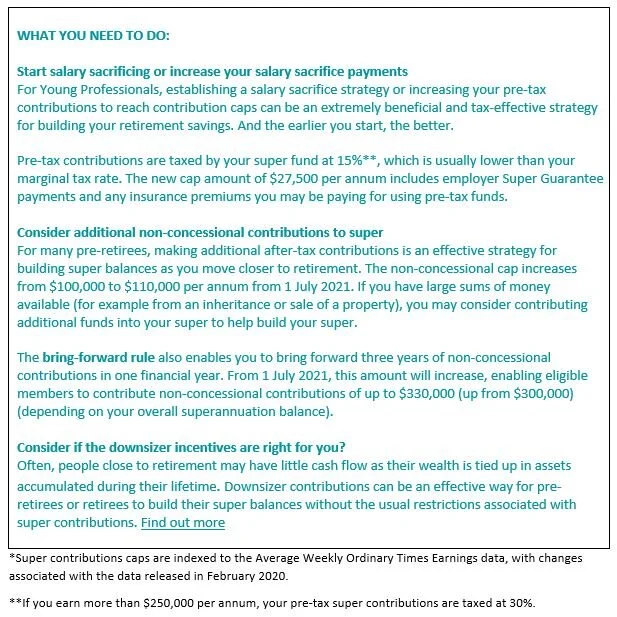

#1: Opportunities to contribute more to super

Super contribution caps, for both Concessional Contributions (pre-tax) and Non-concessional Contributions (after-tax) will increase from 1 July, 2021*.

The Concessional (pre-tax) Contributions Cap will increase from $25,000 to $27,500 per annum.

The Non-concessional (after-tax) Contributions Cap will increase from $100,000 to $110,000 per annum.

Federal Budget 2021-22 announcements, if legislated, also include removing work test requirements and enabling access to non-concessional bring-forward arrangements for Australians aged 67-74 years of age.

The Downsizer Incentive extension was also flagged as part of the Federal Budget 2021-22 announcements. If legislated, the scheme will be extended to include homeowners aged from 60 years, (previously 65 years). The incentive enables after-tax contributions to super of up to $300,000 from the proceeds of the sale of their home. (A couple may contribute a total of $600,000).

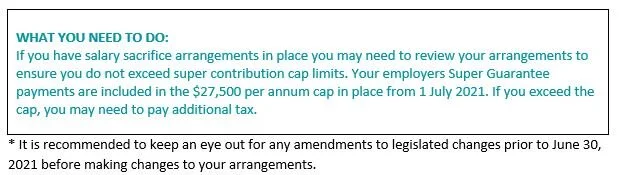

#2: Increases to super guarantee contributions

From 1 July 2021 compulsory Super Guarantee payments paid by employers to employees will increase from 9.5% to 10% of your wages/salary*.

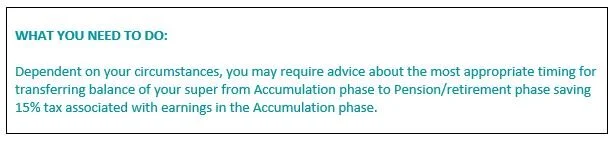

#3 More tax-free income

For retirees, the Transfer Balance Cap is increasing from $1.6 million to $1.7 million from 1 July 2021. The transfer balance cap limits the amount you are able to hold in your ‘Retirement Phase’ or tax-free phase of your super.

The indexation of the Transfer Balance Cap means that a single uniform cap does not apply to everyone, rather a personal transfer balance cap between $1.6 million and $1.7 million will apply.

Any additional funds above the cap amount are able to be held in the ‘Accumulation Phase’ where earnings from your investments are taxed at 15%.

Seeking qualified advice is important when considering your superannuation options, as different strategies can have varied financial and tax implications, which may be more appropriate at different stages of your life and circumstances.

For advice about how you can make the most of the strategies available to you for building your superannuation and for planning your retirement, I encourage you to contact our office on 07 3720 1299 or email admin@wealthfundamentals.com.au

Lane Moses Pty Ltd ABN 56 092 186 117 trading as Wealth Fundamentals and its advisers are Authorised Representatives of Fortnum Private Wealth Ltd ABN 54 139 889 535 AFSL 357306.

The information (including taxation) contained within this document does not consider your personal circumstances and is of a general nature only - unless otherwise stated. Wealth Fundamentals strongly suggests that you should not act on it without first obtaining professional advice specific to your circumstances. This information is based upon our understanding of legislation at the time of writing. Such legislation may be subject to change.

This publication cannot be reproduced in any form without the express written consent of the author.