Now, more than ever, young professionals are looking for wealth accumulation opportunities in response to skyrocketing house prices, low interest rates and concerns of economic performance associated with COVID.

Identifying ways to build wealth is among the most common discussions I have with clients. Here I share three tips for building wealth in uncertain times.

#1: Make use of what you already have

Using a debt recycling strategy, many young professionals have an opportunity to take advantage of equity they may have accumulated in their homes and use it for investing.

This wealth accumulation strategy involves using an investment loan to invest in income producing assets, with the income earned, used to pay down your mortgage. It’s a continual process where the debt in your mortgage (non-deductible debt) is replaced by debt associated with an investment loan (deductible debt).

This strategy can be especially worthwhile during periods of low interest rates and may also have tax advantages.

#2: Super-size it

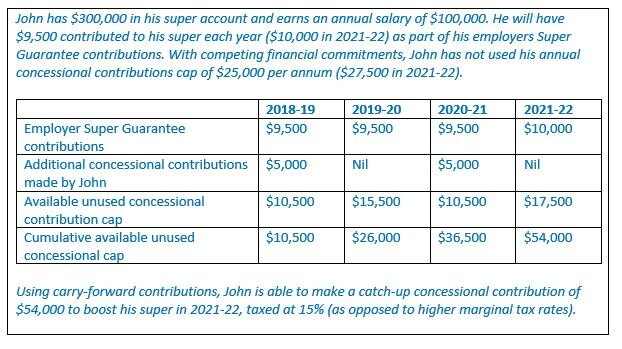

If you have not made the most of salary sacrifice arrangements for the last three years, you have an opportunity to boost your super balance by ‘catching-up’ your unused pre-tax (concessional) super contribution allowances through carry-forward contributions.

Super is a tax-effective way to save for your retirement, with concessional contributions taxed at 15%, rather than marginal tax rates. The scenario below outlines how this strategy can be used to boost your super.

Carry-forward contributions were introduced, enabling you to carry-forward unused annual concessional contribution limits for up to five years. Concessional contributions include employer’s Super Guarantee payments, salary sacrifice contributions or any other personal contributions where a tax deduction is claimed. The 2018-19 financial year was the starting year to be able to accrue your unused cap amount, and to be eligible to take advantage of catch up concessional contributions, you must have super balance less than $500,000 at 30 June in the previous financial year.

#3: Don’t procrastinate… prioritise

Prioritising your long-term wealth is vital and small changes made now to your financial habits could mean you are hundreds of thousands of dollars better off in the future. Simple steps such as understanding your expenses, prioritising your debts, protecting your wealth and starting an investment strategy can make a positive difference to your wealth in the long run, regardless of economic cycles. The most important thing you can do is take action.

The suitability of the utilising wealth accumulation or debt recycling strategies will depend on your personal and financial circumstances. It is important to understand all the risks involve and seek financial advice to determine if any of these strategies are appropriate for you.

For advice about making the most of wealth accumulation strategies for your personal circumstances, I encourage you to contact our office on 07 3720 1299 or email admin@wealthfundamentals.com.au

Lane Moses Pty Ltd ABN 56 092 186 117 trading as Wealth Fundamentals and its advisers are Authorised Representatives of Fortnum Private Wealth Ltd ABN 54 139 889 535 AFSL 357306.

The information (including taxation) contained within this document does not consider your personal circumstances and is of a general nature only - unless otherwise stated. Wealth Fundamentals strongly suggests that you should not act on it without first obtaining professional advice specific to your circumstances. This information is based upon our understanding of legislation at the time of writing. Such legislation may be subject to change.

This publication cannot be reproduced in any form without the express written consent of the author.