Your 40’s and 50’s are important years for making good financial decisions. While you are most likely earning a good income and enjoying your current lifestyle, have you thought about how you can continue that lifestyle in retirement, when you are no longer earning an employment income? Let’s face it, retirement isn’t that far away.

If you haven’t really thought about the future, or deep down you know you are not living within your means, now is the time to do something about it… and you may have more opportunities than you realise.

Small changes made now to your personal cashflow management habits, could mean you are hundreds of thousands of dollars better off in the future.

Cashflow management is not about curtailing your opportunities to enjoy life and strict budgeting – it’s about cashing in on what you’ve got.

Let us help you make the most of opportunities to cash in on your current income

We can help you with savings (and spending) strategies that consider your daily expenditure and lifestyle needs AND fulfil your goals for the future.

#1: Find out where your money is going

Most people are very surprised to find out where they are spending their money. While the usual suspects of your mortgage, fixed costs or investments are well known, it’s the ‘small and often’ spending that is usually a shock. Spending including ATM withdrawals, tap and go purchases and ‘quick’ visits to retail and hardware stores can really add up.The purpose of understanding your expenses is not to stop you spending but to allocate your cash where it is more likely to benefit you in the longer term, such as additional contributions to super or mortgage payments.

#2: Identify how much you will need in retirement

If you want to continue your current level of lifestyle in retirement, you will need an income stream to pay for it. To put it bluntly, if you are currently earning an employment income of $85,000 per year, in retirement you would need a capital base of more than $1.6 million (returning 5%) to achieve the same income.

#3: Simple steps to help you get ahead

Depending on your current circumstances and future financial goals, there are many ways we can help you, including:

• Super strategies: Super is one of the most tax-effective mechanisms for building a retirement income, and strategies such as salary sacrificing and additional contributions can make an enormous difference (as our scenarios below demonstrate).

• Make the most of your debt: Prioritising debt according to interest payable, taking advantage of low interest rates and other strategies such as the use of offset accounts or re-drawing facilities can make a big difference to your financial circumstances.

• Prepare for the unexpected: Protecting your lifestyle and income through personal insurances should be an important part of your financial strategy. If you were unable to work, would you be able to meet your commitments?

• Understanding the what ifs: We can assist you with your financial decision making by using real life scenarios such as amending home loan repayments to highlight the positive impact of your decisions in the long run.

• Finding a better way: By collaborating with other aligned professionals, such as your accountant, we may be able to identify tax efficiencies and more tax-effective ways to structure your debt or manage your investments. It pays to find out.

Cashflow management in action - Scenarios

The scenarios below outline how making additional contributions to super can increase your balance significantly (by more than $100,000 at retirement in this instance).

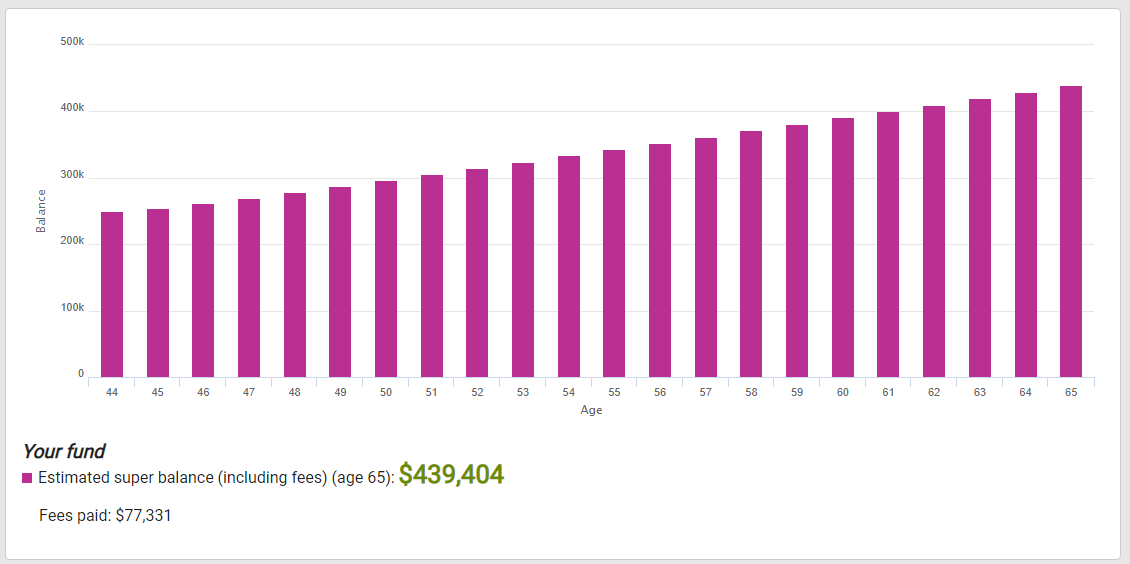

Scenario 1: Nick is 45 years old and has a super balance of $250,000. He earns $85,000 per annum (and his employer pays 9.5% contributions to his super) and he would like to retire at 65.

His estimated balance upon retirement is $439,404.

Scenario 2: Nick is 45 years old and has a super balance of $250,000. He earns $85,000 per annum (and his employer pays 9.5% contributions to his super) and he would like to retire at 65. Nick begins to make additional monthly contributions of $500 to his super (after-tax). Nick’s new estimated super balance upon retirement is $566,903.

{kind=link}

If you would like to know more about opportunities to cash in on your current income to help you live the retirement lifestyle of your choice, I encourage you to contact us today. Phone 07 3720 1299 or email admin@wealthfundamentals.com.au

Lane Moses Pty Ltd ABN 56 092 186 117 trading as Wealth Fundamentals and its advisers are Authorised Representatives of Fortnum Private Wealth Ltd ABN 54 139 889 535 AFSL 357306.

The information (including taxation) contained within this document does not consider your personal circumstances and is of a general nature only – unless otherwise stated. Wealth Fundamentals strongly suggests that you should not act on it without first obtaining professional advice specific to your circumstances. This information is based on our understanding of legislation at the time of writing. Such legislation may be subject to change. This publication cannot be reproduced in any form without the express written consent of the author.