There is good news if the super balance on your recent statement is not what you were hoping for, or if you just know it is time to get serious about your super. You now have a new opportunity to boost your balance.

Just because you have not been in a position to utilise your full contribution caps each year does not mean you have left it too late to make the most of your super.

Super is a tax-effective way to save for your retirement, but if you don’t take advantage of your contribution limits each year, you could be left short when it comes to boosting your super and living the retirement lifestyle of your choice.

The good news is from 1 July 2019, carry-forward contributions mean you can now carry-forward any of your unused annual pre-tax concessional contribution limits ($25,000 per annum), from the 2018/19 financial year onwards, for up to five years.

In addition, the bring-forward rule offers further opportunities to contribute large amounts of money to super as after-tax contributions.

1. Carry-forward contributions – take advantage of unused concessional contribution caps

Carry-forward contributions enable you to ‘catch-up’ your unused concessional contribution allowances over a five year period, helping you to boost your super balance.

Carry-forward contributions can be especially beneficial for business owners, people who work part time or experience time out of the workforce, and therefore make limited super contributions. The new rules can also be beneficial for those who have increased disposable incomes and are looking to boost their super balance, such as families with adult children who are no longer paying school fees and other significant family expenses.

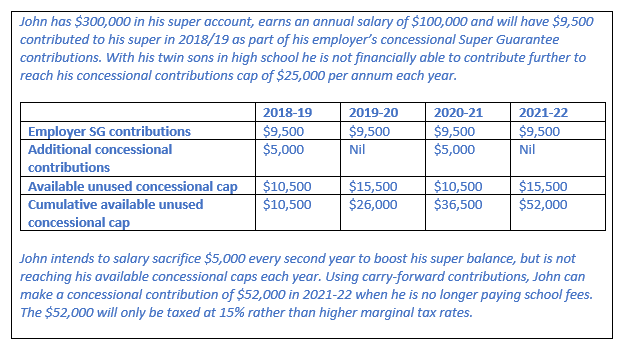

The scenario below explains how carry-forward contributions can be used to boost your super.

The carry-forward contributions are only available for people under 65 years of age who have a super balance less than $500,000 and they only apply to concessional (pre-tax) contributions to super. Concessional contributions include your employer’s 9.5% contributions, salary sacrifice contributions, or personal contributions that you claim a tax deduction for. If you exceed the concessional contributions cap or carry-forward caps, penalties will apply.

2. The ‘bring-forward rule’ – another opportunity to contribute large amounts to super

The bring-forward rule offers you the opportunity to contribute up to $300,000 in one financial year into your super, which may be beneficial if you have large sums of money available (for example from an inheritance or sale of a property).

Annual amounts for after-tax or non-concessional contributions are capped at $100,000 per annum, however utilising the bring-forward rule enables people under 65 years of age to bring forward three years of non-concessional contributions and contribute up to $300,000 in one financial year.

The bring-forward rule can be a useful strategy for people close to retirement who are looking to boost their super balance for making the most of a tax free income stream in their retirement years.

While non-concessional contributions are not subject to tax, if you exceed the annual caps, the excess is taxed at 47%. You are only able to access the full bring-forward rule if you have less than $1.4 million in super. Other restrictions include:

• If you have a super balance between $1.4 and $1.5 million, you are only able to use the bring-forward rule to contribute $200,000 over two years.

• If you have a super balance between $1.5 and $1.6 million, you are not able to utilise the bring-forward rule and can only contribute $100,000 per annum.

• If you have a $1.6 million super balance you are not able to make non-concessional contributions.

If you would like advice on how to make the most of strategies available to you for superannuation or retirement planning, I encourage you to contact our office on 07 3720 1299 or email admin@wealthfundamentals.com.au.

Lane Moses Pty Ltd ABN 56 092 186 117 trading as Wealth Fundamentals and its advisers are Authorised Representatives of Fortnum Private Wealth Ltd ABN 54 139 889 535 AFSL 357306.

The information (including taxation) contained within this document does not consider your personal circumstances and is of a general nature only – unless otherwise stated. Wealth Fundamentals strongly suggests that you should not act on it without first obtaining professional advice specific to your circumstances. This information is based on our understanding of legislation at the time of writing. Such legislation may be subject to change. This publication cannot be reproduced in any form without the express written consent of the author.